From Dirhams to Rupees – How NRIs in Dubai Manage Money Transfers to India

Last month, Priya from Dubai Marina called me with frustration in her voice. She'd been sending AED 8,000 monthly to her parents in Pune for three years using her Emirates NBD bank.

Her latest transfer shocked her - what should have been ₹1,90,000 became ₹1,82,000 after all fees and charges.

"Savitri, I'm losing ₹8,000 every month just on transfer costs. That's nearly ₹1 lakh annually! There has to be a better way."

There absolutely is. After I walked Priya through the strategies I'm sharing in this article, her next transfer of the same AED 8,000 resulted in ₹1,89,200 reaching her parents. She saved ₹7,200 in a single transfer by switching her method and timing.

As someone who's helped over 500 Dubai NRIs optimize their transfers, I can tell you that most are leaving significant money on the table. The difference between smart and average transfer strategies can save you ₹50,000-1,00,000 annually on regular remittances.

By the end of this guide, you'll know exactly which transfer methods Dubai NRIs use, how to time exchange rates like a professional trader, which apps offer genuine value, and the regulatory requirements you must follow.

You'll have a systematic approach to maximize every dirham you send home.

The Dubai-India Transfer Landscape: What's Really Happening

Dubai processes over $15 billion in remittances to India annually, making it one of the largest remittance corridors globally. Yet most NRIs use outdated, expensive methods because they don't understand their options.

The transfer landscape has evolved dramatically. Traditional bank wires that cost AED 100+ in fees now compete with digital services charging AED 10-15. Exchange rate markups have dropped from 3-5% to 0.5-1% for smart users. Transfer times have reduced from 3-5 days to minutes.

But here's what most NRIs miss: the choice of transfer method depends on your specific situation. A software engineer sending AED 5,000 monthly to parents needs different tools than a business owner transferring AED 50,000 quarterly for property investment.

👉 Tip: The "best" transfer method isn't universal - it depends on your transfer frequency, amounts, recipient needs, and timing flexibility.

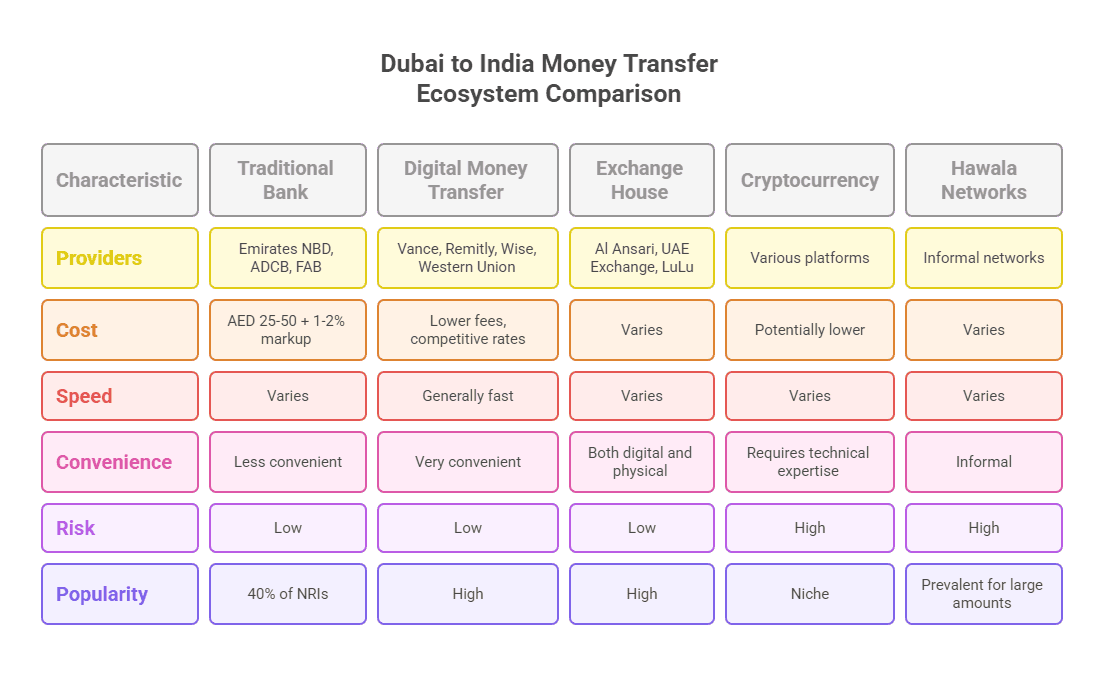

The current Dubai transfer ecosystem offers five main pathways:

Traditional Bank Transfers: Still used by 40% of NRIs despite high costs. Emirates NBD DirectRemit, ADCB, and FAB offer this service with AED 25-50 fees plus 1-2% rate markups.

Digital Money Transfer Services: Vance, Remitly, Wise, and Western Union dominate this space with lower fees and competitive rates.

Exchange House Services: Al Ansari Exchange, UAE Exchange, and LuLu Exchange provide both digital and physical transfer options.

Cryptocurrency Routes: Growing but still niche, offering potentially lower costs but requiring technical expertise.

Hawala Networks: Informal but still prevalent, especially for larger amounts, though carrying legal risks.

Each method has specific advantages, and the smartest NRIs often use 2-3 different services depending on the transfer purpose and market conditions.

Exchange Rate Timing: The Science Behind Smart Transfers

The AED-INR exchange rate can fluctuate 2-4% within a month, meaning a AED 10,000 transfer could result in ₹2,000-8,000 difference based purely on timing. Understanding these patterns is crucial for maximizing your transfers.

Current exchange rate analysis shows AED-INR trading around 23.85-24.20 in 2025, with forecasts suggesting gradual strengthening toward 24.50-25.00 by late 2025. The UAE's economic diversification and India's growth trajectory support this trend.

Here are the timing patterns smart Dubai NRIs follow:

Monthly Patterns: The first week typically shows stronger rates due to salary inflows and corporate transfers. Mid-month often sees slight weakness as supply increases.

Seasonal Trends: December-January sees high demand due to holiday remittances, often weakening rates. March-April shows strength due to financial year-end planning.

Economic Event Impact: RBI policy announcements, UAE economic data releases, and oil price movements create short-term volatility that smart transferers exploit.

👉 Tip: Set up rate alerts at your target levels rather than trying to predict perfect timing. Aim for the top 20% of rates rather than the absolute peak.

The Rate Alert Strategy

I recommend Dubai NRIs set three rate thresholds:

Target Rate: Your ideal rate based on 3-month historical highs. Transfer 50% of planned amounts when this hits.

Acceptable Rate: 1-2% below target rate. Transfer 30% of planned amounts here.

Emergency Rate: 3-4% below target. Only transfer urgent amounts, delay non-essential transfers.

This approach ensures you capture good rates without trying to time the market perfectly.

Factors Driving AED-INR Movement

Understanding what moves exchange rates helps you anticipate favorable periods:

Oil Prices: Higher oil strengthens AED as UAE benefits from increased revenue. Watch crude oil trends for medium-term direction.

RBI Policy: Interest rate changes, intervention patterns, and inflation targeting affect INR strength. Follow RBI announcements closely.

UAE Economic Data: GDP growth, non-oil sector performance, and tourism numbers influence AED demand.

Global Risk Sentiment: During uncertainty, investors prefer stable currencies like AED over emerging market currencies like INR.

The App Revolution: Which Platforms Dubai NRIs Actually Use

The money transfer app landscape has exploded, but only a few consistently deliver value for Dubai-India transfers. Based on my analysis of actual user experiences and costs, here's what works:

Vance: The Google-Rate Champion

Vance has become the go-to choice for many Dubai NRIs because they offer "Google rates" - essentially the mid-market rate with minimal markup. Their partnership with LuLu Exchange and RBI-regulated banks ensures reliability.

Key Features:

- Real-time market rates with no hidden markups

- 24/7 human customer support

- Bank account and cash pickup options

- Transfer completion within minutes

- No minimum transfer amounts

Best For: Regular senders who prioritize rate transparency and speed.

Cost Example: AED 5,000 transfer typically results in ₹1,19,400 (at 23.88 rate) with AED 10 fee.

Remitly: The Reliability Choice

Remitly offers two service tiers - Express (minutes) and Economy (1-3 days). Their economy option provides excellent rates, while express serves urgent needs.

Key Features:

- New customer bonuses and promotional rates

- Multiple delivery options including UPI

- Strong customer service in multiple languages

- Guaranteed delivery times with fee refunds for delays

Best For: NRIs who want flexibility between speed and cost.

Cost Example: AED 5,000 economy transfer at ₹1,19,000 with AED 12 fee, express at ₹1,18,600 with AED 25 fee.

Wise (Formerly TransferWise): The Transparent Pioneer

Wise revolutionized transparency by showing exactly how they make money. They use real exchange rates and charge clear, upfront fees.

Key Features:

- Real exchange rate (no markup)

- Clear fee structure

- Multi-currency accounts for advanced users

- Strong regulatory compliance across multiple countries

Best For: Financially sophisticated users who value complete transparency.

Cost Example: AED 5,000 transfer at market rate (say 23.90) with AED 18 fixed fee.

Al Ansari Exchange: The Traditional Choice

As UAE's largest exchange house, Al Ansari combines traditional reliability with digital convenience. Their 260+ branches provide backup for digital services.

Key Features:

- 50+ years of remittance experience

- Physical branch network for complex transactions

- Competitive rates on larger amounts

- Cash Express for instant transfers

Best For: Older NRIs comfortable with traditional services or those making large transfers.

👉 Tip: Compare live rates across 3-4 services before each transfer. Rate differences can vary significantly based on market conditions and transfer amounts.

Hidden Costs Analysis: What Banks Don't Tell You

Traditional bank transfers appear simple but hide multiple cost layers that smart NRIs avoid:

Emirates NBD DirectRemit Cost Breakdown

Advertised: AED 26.25 flat fee (recently updated from free)

Hidden Reality:

- Exchange rate markup: 1.5-2% (AED 150-300 on AED 15,000 transfer)

- Correspondent bank charges: AED 50-150 depending on receiving bank

- Receiving bank charges in India: ₹200-500 for international wires

Total Hidden Costs: AED 200-450 on a AED 15,000 transfer, or 1.3-3% total cost.

Digital Service Cost Transparency

Leading apps have forced transparency, but comparison requires understanding their models:

Fixed Fee Model (Wise, Vance): Clear fee structure, market exchange rates.

Rate Markup Model (Western Union, Some UAE Exchange): Lower/no fees, but worse exchange rates.

Hybrid Model (Remitly, MoneyGram): Combination of fees and slight rate markups.

Real Cost Comparison Table

Service | AED 5,000 Transfer | Exchange Rate | Fees | Total INR Received |

|---|---|---|---|---|

Emirates NBD | 23.65 | AED 75 | ₹1,17,325 | AED 150 (3.0%) |

Vance | 23.88 | AED 10 | ₹1,19,390 | AED 20 (0.4%) |

Wise | 23.90 | AED 18 | ₹1,19,482 | AED 28 (0.6%) |

Remitly Economy | 23.85 | AED 12 | ₹1,19,238 | AED 32 (0.6%) |

👉 Tip: Always calculate the total INR received, not just advertised fees. A service with higher fees but better rates often delivers more money.

Speed vs Savings: Finding Your Transfer Strategy

Dubai NRIs face a fundamental choice: maximize money received or minimize transfer time. Understanding this trade-off helps optimize your approach.

The Speed Spectrum

Instant Transfers (0-30 minutes):

- Premium services: Vance Express, Remitly Express

- Cost: Additional 0.3-0.8% in fees or worse rates

- Use for: Medical emergencies, urgent payments, last-minute needs

Fast Transfers (1-4 hours):

- Standard digital services: Vance, Wise, Al Ansari digital

- Cost: Baseline rates and fees

- Use for: Regular remittances, planned expenses

Economy Transfers (1-3 days):

- Budget options: Remitly Economy, some bank transfers

- Cost: Best rates, lowest fees

- Use for: Planned investments, non-urgent family support

Smart Transfer Scheduling

Experienced Dubai NRIs use a three-tier approach:

70% Regular Schedule: Monthly/bi-weekly transfers using fast services at good rates. Set up automatic transfers when rates are favorable.

20% Opportunistic: Larger transfers when exchange rates hit target levels, using economy services for maximum value.

10% Emergency Reserve: Instant transfer capability for genuine emergencies, accepting higher costs for speed.

This approach balances cost optimization with practical needs.

👉 Tip: Use calendar reminders to check rates weekly rather than daily. Daily monitoring leads to poor timing decisions due to noise in rate movements.

Regulatory Framework: Staying Compliant Across Borders

UAE and Indian regulations for money transfers are straightforward but strictly enforced. Non-compliance can result in account freezes, penalties, or legal complications.

UAE Regulations

No Transfer Limits: UAE doesn't restrict outbound personal remittances, but banks may have internal limits.

Source of Funds: All transfers must be from legitimate income. Banks may request salary certificates for large amounts.

Documentation: Emirates ID, passport, and proof of UAE residence required. Some services require additional KYC for amounts over AED 15,000.

AML Compliance: Structured transactions (breaking large amounts into smaller transfers) to avoid reporting requirements can trigger investigations.

Indian Regulations

Liberalized Remittance Scheme (LRS): Indian residents can receive unlimited personal remittances without RBI approval.

Tax Implications: Amounts over ₹50,000 annually may require reporting in Indian tax returns, depending on purpose.

Banking Compliance: Indian banks report foreign remittances to tax authorities. Keep records of transfer purposes.

FEMA Compliance: NRI recipients must follow Foreign Exchange Management Act guidelines for investment or business-related transfers.

Documentation Best Practices

Transfer Records: Maintain detailed records including transfer receipts, exchange rates, and purposes.

Tax Documentation: Keep transfer records for 7 years to support Indian and UAE tax filings if required.

Compliance Letters: For large investments from transfer proceeds, obtain CA letters confirming compliance with regulations.

👉 Tip: For transfers above AED 50,000, consult with a CA familiar with NRI regulations to ensure proper documentation and compliance.

Tax Implications: What Dubai NRIs Must Know

Dubai's tax-free status doesn't eliminate all tax considerations for international transfers. Understanding implications on both sides prevents costly mistakes.

UAE Tax Considerations

No Personal Tax: Dubai NRIs pay no income tax on salary or investment returns, including from Indian transfers.

VAT Impact: Some money transfer services charge 5% VAT on fees (not transfer amounts). Factor this into cost calculations.

Business Transfers: If transferring for business purposes, additional documentation and potentially corporate regulations apply.

Indian Tax Implications

Recipient Tax: Generally, personal remittances to Indian residents aren't taxable income for recipients.

Investment Proceeds: If transferred funds are used for investments in recipient's name, tax implications depend on investment type and returns.

Reporting Requirements: Large transfers may require recipients to report sources in their Indian tax returns.

Gift Tax Rules: NRI gift tax regulations apply if transfers are considered gifts rather than family support.

Transfer Purpose Planning

Family Maintenance: Regular support to parents/spouse typically has no tax implications for recipients.

Property Investment: Transfers for Indian property purchases require proper documentation and may affect both parties' tax positions.

Business Investment: Commercial transfers have different compliance requirements and tax implications.

Education/Medical: These purposes often receive favorable treatment but require supporting documentation.

👉 Tip: Maintain clear records of transfer purposes. "Family support" is straightforward, but investment-related transfers may require additional documentation.

Security Protocols: Protecting Your Cross-Border Transfers

Money transfer security involves multiple layers - choosing regulated services, following safe practices, and protecting personal information.

Service Selection Security

Regulatory Licenses: Only use services licensed by UAE Central Bank and/or RBI. Check license numbers on their websites.

Insurance Coverage: Leading services provide transfer insurance or guarantees. Understand what's covered.

Data Encryption: Verify services use bank-grade SSL encryption for all transactions and data storage.

Track Record: Choose established services with years of operation and positive customer reviews from verified users.

Personal Security Measures

Device Security: Only use transfer apps on secure, updated devices. Avoid public WiFi for financial transactions.

Authentication: Enable two-factor authentication where available. Use strong, unique passwords.

Transfer Verification: Always verify recipient details before confirming transfers. Mistakes are difficult to reverse.

Receipt Management: Save all transfer confirmations and track transfers until completion.

Fraud Prevention

Phishing Protection: Legitimate services never ask for passwords or OTPs via email or phone calls.

Rate Verification: Compare offered rates against live market rates. Deals "too good to be true" usually are.

Advance Fee Scams: Never pay upfront fees to unlock better rates or faster transfers from unknown services.

Social Engineering: Be cautious of "friends" recommending unlicensed services or unofficial channels.

👉 Tip: If a transfer service asks for your bank login credentials or offers rates significantly better than market leaders, it's likely fraudulent.

Common Transfer Mistakes Dubai NRIs Make

After analyzing hundreds of NRI transfer patterns, certain mistakes appear repeatedly. Learning from others' errors saves significant money and frustration.

Mistake 1: Banking Loyalty Despite High Costs

Many NRIs stick with their salary bank for transfers due to familiarity, despite paying 2-3% extra in total costs. This loyalty costs AED 2,000-6,000 annually for regular senders.

Solution: Evaluate transfer costs separately from banking relationships. Use your bank for UAE services but optimize transfers independently.

Mistake 2: Ignoring Rate Timing

Transferring immediately when money arrives in salary accounts, regardless of exchange rates, costs 1-3% annually due to poor timing.

Solution: Unless urgent, wait for favorable rates within your acceptable range. Set up rate alerts for automatic notifications.

Mistake 3: Not Comparing Total Costs

Focusing only on advertised fees while ignoring exchange rate differences and hidden charges leads to poor service selection.

Solution: Calculate total INR received for identical AED amounts across different services before choosing.

Mistake 4: Irregular Large Transfers

Sending large amounts irregularly (AED 20,000 quarterly vs AED 5,000 monthly) often results in poor average rates and higher total costs.

Solution: Consider more frequent, smaller transfers for better rate averaging, unless you have strong rate timing skills.

Mistake 5: Inadequate Documentation

Poor record-keeping of transfer purposes, receipts, and compliance documentation creates problems during tax filing or regulatory inquiries.

Solution: Maintain organized transfer records including purpose, exchange rates, fees, and recipient confirmations.

👉 Tip: Review your transfer costs annually. If you're spending more than 1% of transferred amounts in total costs, you're likely using suboptimal methods.

Advanced Timing and Rate Strategies

Sophisticated Dubai NRIs use advanced techniques to optimize their transfers beyond basic rate watching.

The Dollar-Cost Averaging Approach

Instead of trying to time perfect rates, systematic transferers send fixed AED amounts at regular intervals, averaging out rate volatility over time.

Example Strategy:

- Target: AED 60,000 annually to family

- Method: AED 5,000 monthly transfers regardless of rates

- Benefits: Eliminates timing stress, achieves average rates, ensures consistent family support

Results: Over 12-24 months, this typically achieves rates within 1-2% of optimal timing while requiring zero market monitoring.

The Split Strategy

Advanced users split transfers based on urgency and market conditions:

50% Systematic: Regular amounts transferred on fixed schedule for essential needs 30% Tactical: Larger amounts transferred during favorable rate periods

20% Opportunistic: Flexible transfers when exceptional rates occur

Rate Pattern Recognition

Experienced transferers track patterns:

Weekly Patterns: Tuesday-Thursday often show different rates than Monday/Friday due to banking cycles

Monthly Patterns: First week typically stronger, mid-month weaker due to flow patterns

Seasonal Patterns: Festival seasons, monsoon periods, and financial year-ends create predictable volatility

The Forward Rate Strategy

Some sophisticated users work with exchange houses to lock forward rates for future transfers, though this requires larger amounts and financial expertise.

👉 Tip: Start with systematic transfers for 70% of your needs, then gradually add tactical elements as you understand rate patterns better.

Future of NRI Transfers: What's Coming Next

The Dubai-India transfer landscape continues evolving rapidly. Understanding upcoming changes helps you prepare and potentially benefit from new opportunities.

Technology Developments

Blockchain Integration: Several services are piloting blockchain-based transfers promising lower costs and faster settlement.

Central Bank Digital Currencies (CBDCs): Both UAE and India are developing digital currencies that could revolutionize cross-border transfers.

AI-Powered Rate Prediction: Advanced algorithms will provide better rate forecasting, helping users optimize timing.

Open Banking Integration: Direct bank-to-bank transfers without intermediaries may reduce costs further.

Regulatory Evolution

Enhanced Compliance: Expect stricter KYC requirements and better cross-border information sharing between UAE and Indian authorities.

Simplified Processes: Digital-first regulations will likely streamline documentation and approval processes.

Consumer Protection: Stronger regulations protecting transfer users, including guaranteed delivery times and compensation for delays.

Market Competition

New Entrants: Cryptocurrency companies and fintech startups continue entering the market with innovative solutions.

Bank Response: Traditional banks are upgrading their services to compete with digital alternatives.

Fee Compression: Increasing competition will likely drive transfer costs even lower over time.

Investment Integration

Services are beginning to integrate transfers with Indian investment opportunities, allowing NRIs to transfer and invest in single transactions.

👉 Tip: Stay updated on new transfer services and technologies, but don't switch immediately. Let new services prove reliability before transferring from tested options.

Setting Up Your Optimal Transfer System

Now that you understand the complete landscape, here's how to establish your personalized transfer system:

Step 1: Assess Your Transfer Profile

Transfer Frequency: Monthly, quarterly, or irregular

Transfer Amounts: Average and maximum amounts you send

Recipient Needs: Bank account, cash pickup, or UPI delivery preferences

Urgency Tolerance: How often you need instant vs. economy transfers

Rate Sensitivity: Your comfort level with rate timing decisions

Step 2: Select Your Service Mix

Primary Service: Choose one reliable service for 70% of your transfers based on your typical amounts and speed needs.

Secondary Service: Select a backup service with different strengths (perhaps better rates for larger amounts or faster delivery).

Emergency Service: Identify an instant transfer service for genuine emergencies, even if costs are higher.

Step 3: Set Up Rate Monitoring

Rate Alert Levels: Set alerts at your target, acceptable, and minimum rates using apps or services like XE Currency.

Review Schedule: Weekly rate checks for active transferers, monthly for occasional users.

Record Keeping: Maintain spreadsheets or apps tracking your transfer history, rates achieved, and total costs.

Step 4: Establish Transfer Discipline

Budget Integration: Include transfer costs in your monthly budget planning.

Timing Rules: Define when you'll wait for better rates vs. transfer immediately.

Documentation System: Organize transfer receipts, purposes, and compliance records systematically.

👉 Tip: Spend a weekend setting up your complete system, then follow it consistently rather than making ad hoc decisions each time you need to transfer money.

Your transfer optimization system should be simple enough to follow consistently but sophisticated enough to capture most available savings.

The goal isn't perfect optimization - it's reliable, cost-effective transfers that support your financial goals across both countries.

Ready to optimize your Dubai to India transfers? Compare live rates across multiple services and start saving on every transfer. Join thousands of smart NRIs who have transformed their cross-border money management through strategic planning and the right service selection.

Comments

Your comment has been submitted